A federal tax credit that sat mostly untouched for two decades just became four times more valuable for small businesses, and most employers still have not claimed it.

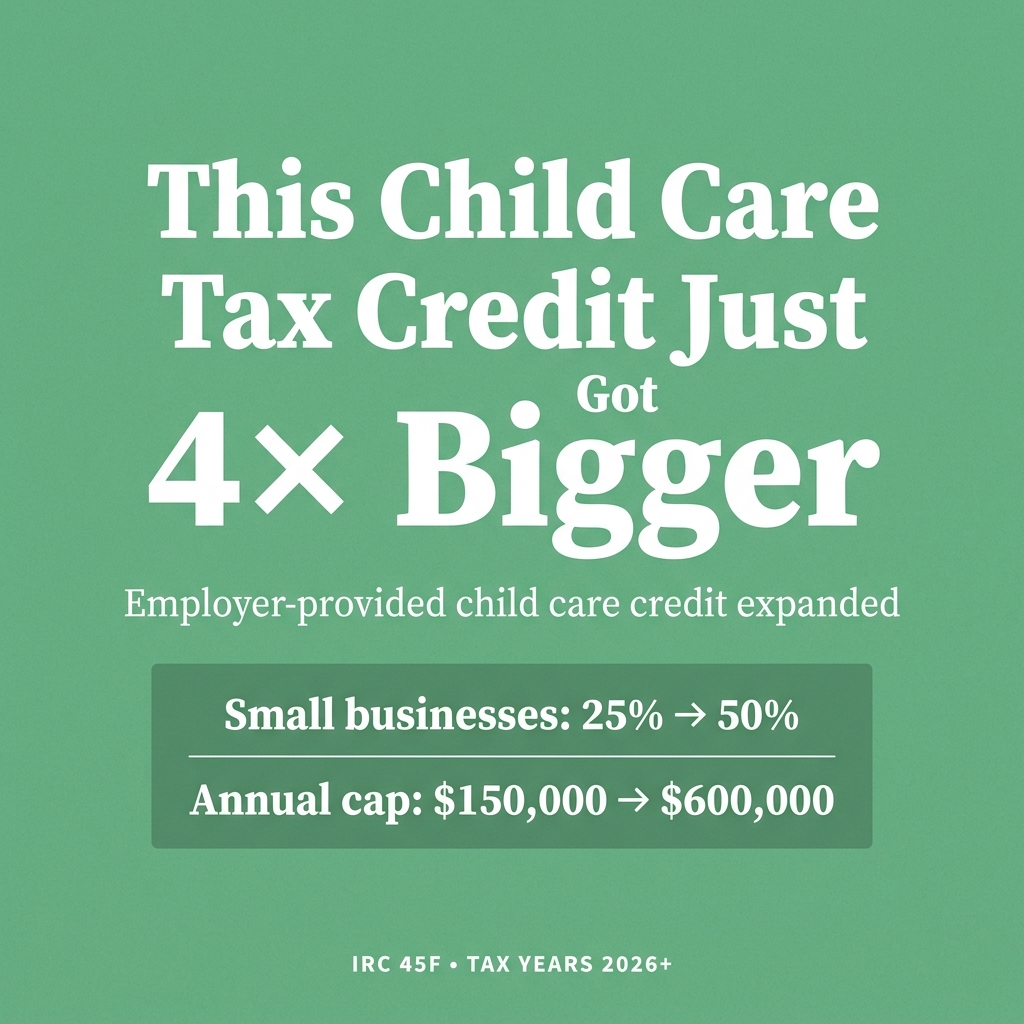

The Employer-Provided Child Care Credit under Section 45F of the Internal Revenue Code was overhauled by the One Big Beautiful Bill Act, signed into law on July 4, 2025. For tax years beginning after December 31, 2025, eligible small businesses can now claim a credit worth 50% of qualified child care expenses, up from the old rate of 25%. The annual cap jumped from $150,000 to $600,000.

For larger employers, the credit is 40% of qualifying expenses with a $500,000 cap. Both thresholds will adjust for inflation starting in 2027.

Who qualifies as a small business

To access the higher 50% rate and $600,000 cap, a business must meet the gross receipts test under IRC Section 448(c). That generally means average annual gross receipts of $32 million or less over the preceding five years, according to the IRS guidance page. S-corps, C-corps, partnerships, LLCs, and sole proprietors all qualify, so long as they are for-profit entities with some federal tax liability.

What counts as a qualifying expense

The law broadened the range of eligible spending beyond building an on-site daycare. Qualifying expenditures now include contracting with licensed third-party child care providers, paying intermediary organizations that coordinate care across multiple providers, and jointly owning or operating facilities with other businesses. Resource-and-referral costs, like helping employees find available care, also qualify at a 10% credit rate.

That pooling provision is significant. Several small employers in the same area can share a facility or a provider contract and each still claim the credit individually, according to Bipartisan Policy Center guidance.

There are limits to watch. The credit is nonrefundable, meaning it can only reduce your tax bill to zero but will not generate a refund. Claiming the credit also reduces the deductible portion of those same expenses. And if you build or acquire a child care facility, there is a 10-year recapture window. Shut the facility down in year 4, and you could owe back 80% of the credit.

Employers claim the credit using IRS Form 8882, filed with their regular business tax return. Unused credits can carry back one year and forward up to 20 years under the general business credit rules.

Historically, only about $18 million in 45F credits was claimed per year across all filers. Treasury is still expected to release additional implementation guidance, particularly around how intermediary contracts and jointly operated facilities will be documented. Businesses considering this credit should work with a tax advisor now to set up proper expense tracking for the 2026 tax year.