The Financial Crimes Enforcement Network (FinCEN), the Treasury Department unit that enforces anti-money-laundering rules, issued an order on February 13, 2026 that removes the requirement for banks to verify the beneficial owners of a business every time it opens a new account. The order, numbered FIN-2026-R001, took effect immediately.

Until now, a rule on the books since 2016 required banks, credit unions, broker-dealers, and other covered financial institutions to collect and verify beneficial ownership information, meaning the identities of anyone who owns 25% or more of a legal entity, or who controls it, at every single account opening. That applied even if the bank had just verified the exact same information days earlier for the same customer.

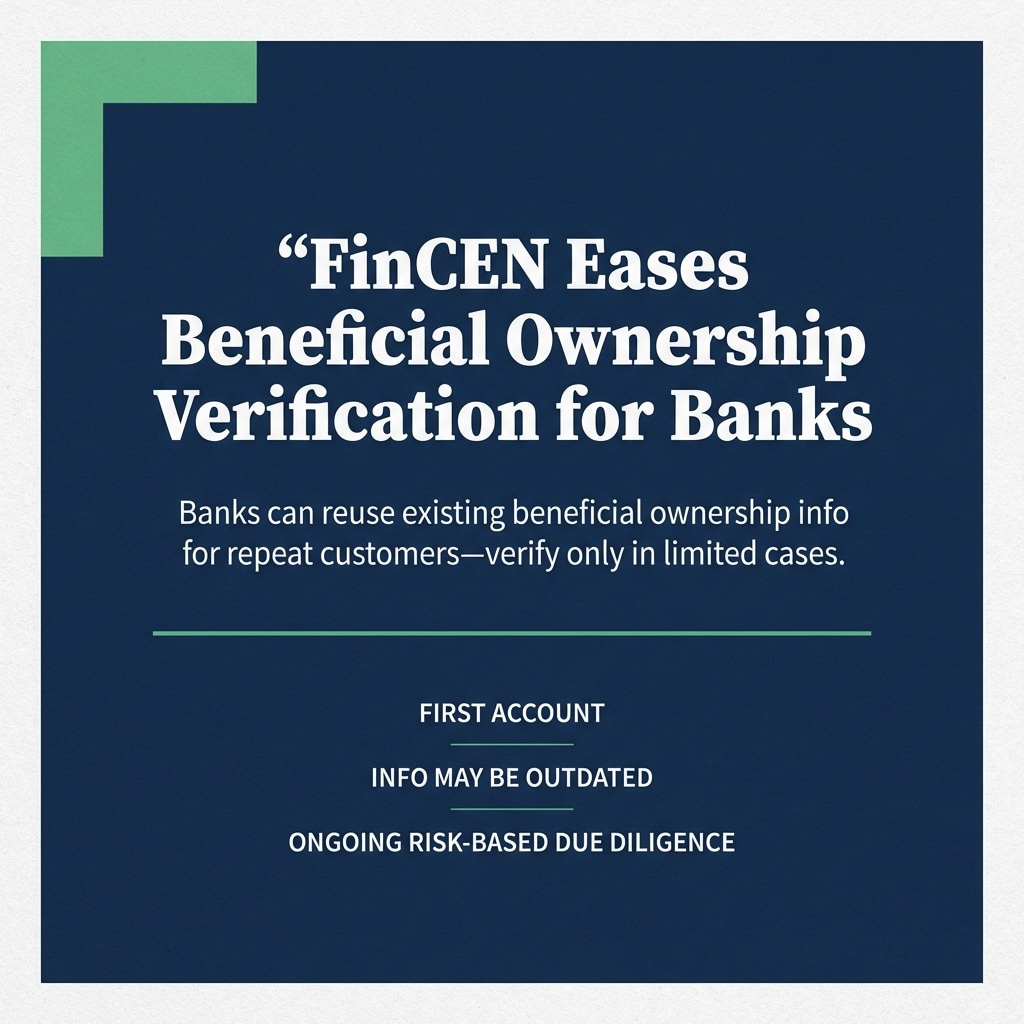

Under the new order, banks only need to verify beneficial owners in three situations. First, when a business customer opens its very first account at the institution. Second, when the bank has reason to believe the ownership information it already has on file may no longer be accurate. And third, as part of the bank’s own risk-based ongoing due diligence procedures.

For existing customers opening additional accounts, the bank can simply rely on the ownership information it already collected, as long as the customer confirms, verbally or in writing, that the information is still correct.

For small businesses, this is a practical improvement. If you already bank somewhere and want to open a second checking account, a line of credit, or a merchant services account, you should no longer need to fill out the same ownership paperwork again from scratch. The American Bankers Association noted that U.S. banks open between 140 and 160 million new accounts every year, and called the change a step toward a more efficient regulatory approach.

There are a few things to keep in mind. This relief is optional for banks. Some institutions may choose to keep requiring full verification at every account opening based on their own risk assessments. If you cannot confirm that your previously filed ownership information is still accurate, your bank must go through the full verification process. And all other Bank Secrecy Act requirements, including suspicious activity monitoring and recordkeeping, remain in place.

If your business ownership has changed since you last opened an account, let your bank know right away. Providing outdated information, even unintentionally, could create compliance problems for both you and your financial institution.

FinCEN has signaled that additional changes to the 2016 Customer Due Diligence Rule are coming through the formal rulemaking process. This order is one piece of a broader effort to modernize anti-money-laundering compliance under the Corporate Transparency Act.